Production report in 1s 8.3. Accounting for finished products in "1C: Accounting"

Accounting for production costs in the program "1C: Accounting 8" is carried out in the context of product groups (types of activity). Previously, they must be entered in the reference book "Nomenclature groups" ( menu: "Enterprise - Goods (materials, products, services)").Example:

Direct production costs are accounted for on accounts 20 "Main production" and 23 "Auxiliary production". This includes everything that can be attributed to specific types of manufactured products (semi-finished products, production services): raw materials written off for production, depreciation of capital equipment, wages and taxes from the payroll of production workers, as well as some services.

During the month, direct costs are reflected in the program with the help of such documents as “Request-invoice”, “Receipt of goods and services” (tab “Services”), “Expense report” (tab “Other”), “Payroll”, as well as regulatory operations "Depreciation and depreciation of fixed assets", "Calculation of taxes (contributions) from payroll" and some others. You should pay attention to the correct indication of the item group both in the documents and in the ways of reflecting depreciation costs and reflecting wages in accounting.

Examples of direct production costs

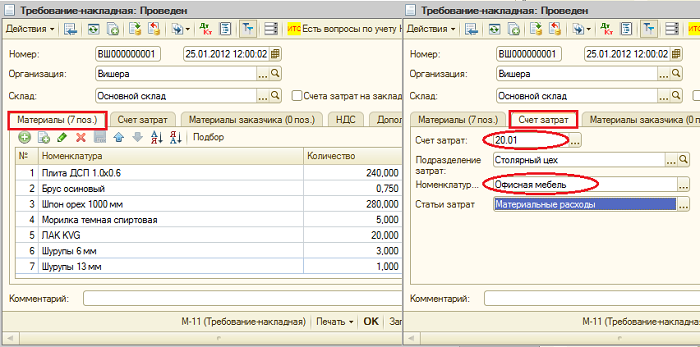

The document "Requirement-invoice" (menu or tab "Production") reflects the write-off of materials to production. The cost account and analytics are listed on the Cost Account tab. When posting the document, the posting Dt 20.01 Kt 10 will be generated, with the corresponding analytics of account 20 (subdivision, item group, cost item).

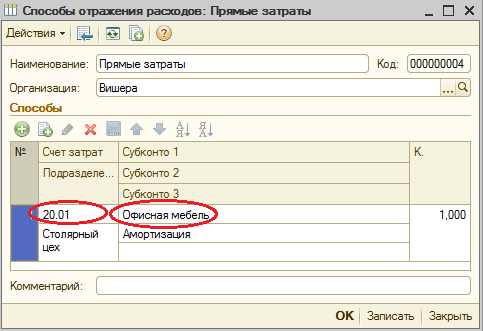

The method of reflecting depreciation expenses (menu or tab "OS" or "Intangible assets"). If you choose this method when accepting a fixed asset for accounting (acceptance for accounting of intangible assets, putting work clothes into operation), then depreciation for this asset (depreciation of intangible assets, repayment of the cost of work clothes) will be charged to the specified account and cost analytics. In this case, the posting Dt 20.01 Kt 02.01 will be generated.

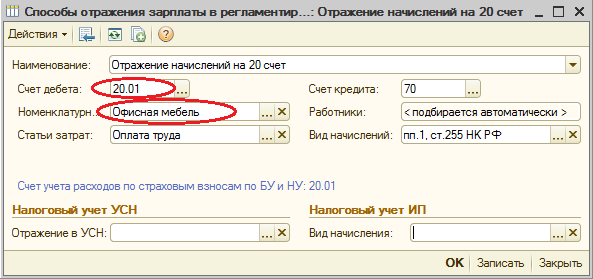

Method of reflecting salary in accounting (menu or tab "Salary"). If you specify this method in the accrual, then the employee's salary and payroll taxes will be charged to the corresponding account and cost analytics. In this case, when calculating the salary, the posting Dt 20.01 Kt 70 will be generated.

At the end of the month, direct costs collected on accounts 20 and 23 are distributed between manufactured products and work in progress by item groups (types of activity). Distribution occurs with the help of regular month-end closing operations.

In addition, there are general production and general business expenses, which are accounted for, respectively, on accounts 25 and 26.

General production expenses during the month are charged to account 25. To reflect them, the same documents can be used as for reflecting direct costs. At the end of the month, the costs collected on account 25 are distributed to account 20 by item groups (types of activity), within a specific unit, in accordance with the distribution base, using routine operations.

General business expenses during the month are charged to account 26. To reflect them, the same documents can be used as for reflecting direct costs. At the end of the month, the write-off of expenses collected on account 26 can occur in two ways. They can be distributed to account 20 by item groups (types of activity) of the entire enterprise, in accordance with the selected distribution base. Or, if the "direct costing" method is used, general business expenses are written off directly to account 90.08 "Administrative expenses" in proportion to the sales proceeds.

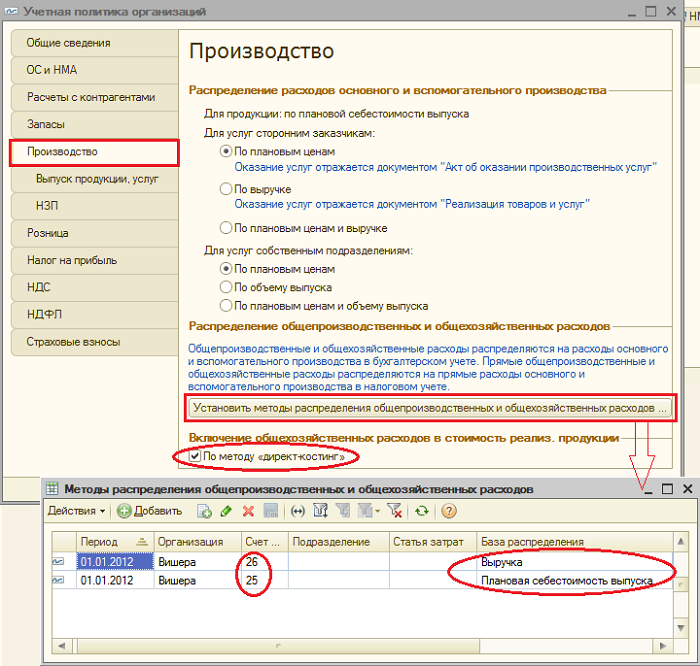

Cost accounting is set up in the form of the organization's accounting policy (menu or tab "Enterprise").

On the “Production” tab, methods for distributing general and general production costs are indicated using the “Set distribution methods ...” button. In the form that opens, you need to indicate the distribution base for each account, which can be the volume of output, the planned cost of production, wages, material costs, revenue, direct costs, and individual items of direct costs. If necessary, you can detail the methods of distribution by departments and cost items.

Here you can also configure the use of the direct costing method and the distribution of production costs for services.

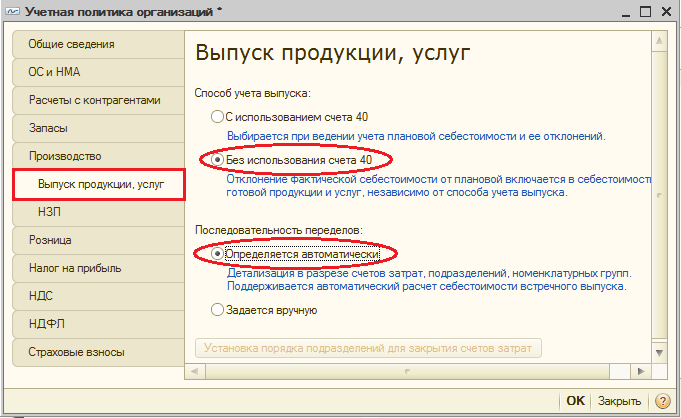

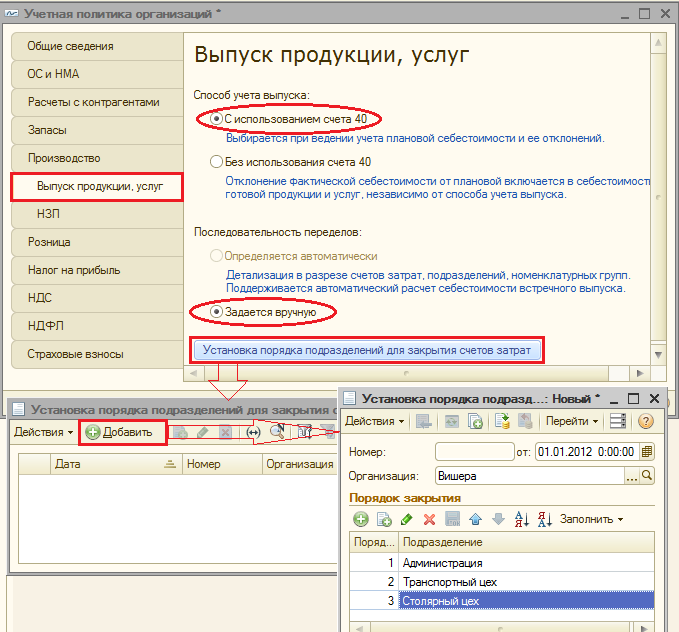

On the “Product output” tab, a method for accounting for the output of finished products (semi-finished products, production services) is selected - with or without the use of account 40. Here it is also necessary to set the definition of the sequence of redistribution for closing accounts, which is important in multi-refining production. Selecting automatic detection is recommended. If the output is accounted for at the planned cost using account 40, then automatic calculation of the sequence of redistribution is not possible. In this case, you need to select the manual method, and then manually set the order of departments for closing accounts (by clicking the button).

Automatic determination of the sequence of redistributions is set:

Manual determination of the sequence of redistributions is set, the order of divisions is established:

Release and sale of finished products

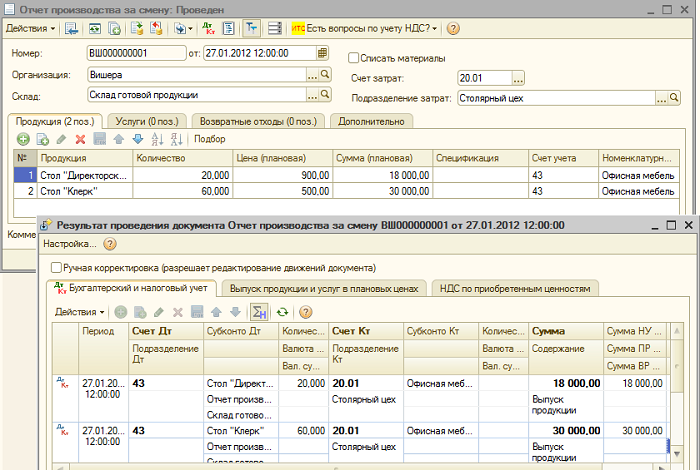

The output of products (semi-finished products, production services for sob. subdivisions) is reflected in the program by the document “Report of production for a shift” (menu or tab “Production”). Released products are accounted for at the planned cost, the document generates posting Dt 43 Kt 20 (or, if the use of account 40 is specified, posting Dt 43 Kt 40). You must correctly specify the item group for the released products.The document "Report of production for the shift" and the result of its implementation (account 40 is not used):

For the correct calculation of the cost in the program, it is necessary to observe the principle of matching income and expenses in the context of product groups (types of activity). That is, if there are costs for an item group, they must correspond to the output and income for this item group.

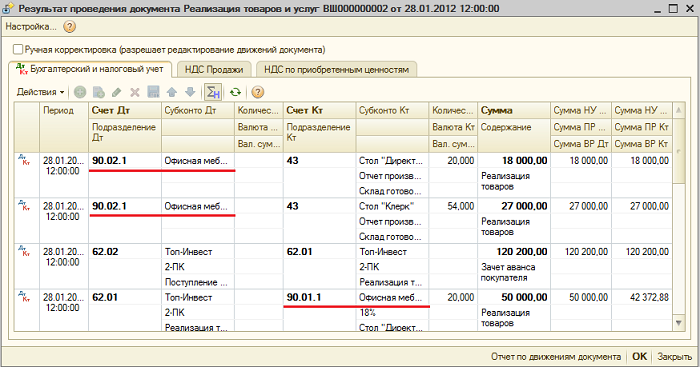

The sale of finished products is reflected in the document “Sales of goods and services”, while generating a revenue entry: Dt 62 Kt 90.01, and a posting to write off the cost of sales: Dt 90.02 Kt 43. Analytics of accounts 90.01 and 90.02 - nomenclature groups (types of activity).

The result of the document for the sale of products:

Closing the period and calculating the actual cost

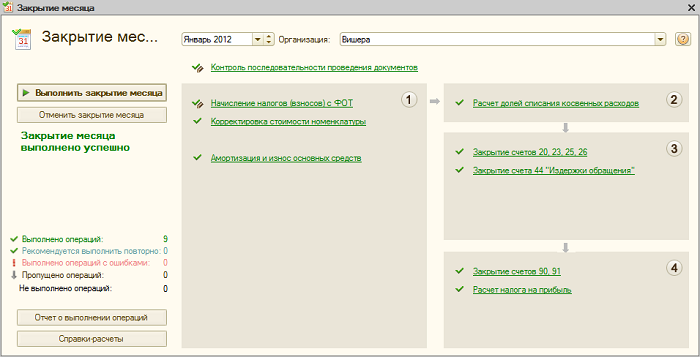

Closing of cost accounts and calculation of the actual cost of manufactured products (semi-finished products) is carried out at the end of the month by routine operations. Preliminary, routine operations must be performed to accrue depreciation of fixed assets and intangible assets, pay off the cost of workwear, write off deferred expenses, calculate salaries and payroll taxes.You can use the routine processing "Closing the month" ( menu: "Operations"). In this case, the program itself will “determine” which scheduled operations are necessary and will carry them out in the correct sequence. Execution occurs on the button "Perform closing of the month".

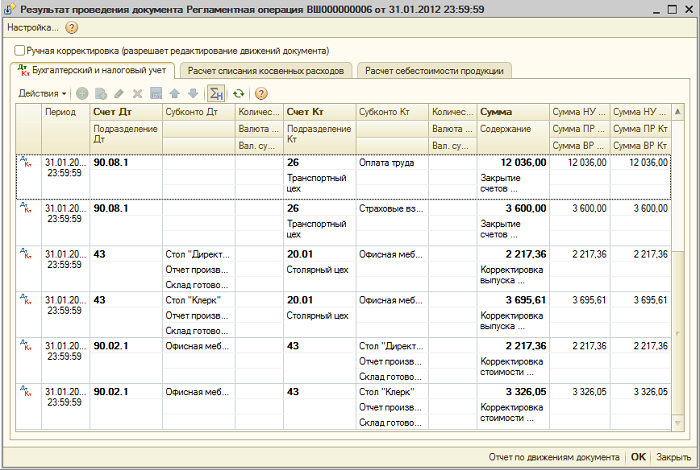

When carrying out the routine operation “Closing accounts 20, 23, 25, 26”, several stages are performed: distribution of indirect costs (according to the established “Distribution Methods”), calculation of direct costs for each product and for each division, cost adjustment.

Let us give an example of the operation “Closing accounts 20, 23, 25, 26” (the organization uses the “direct costing” method). There are postings for closing account 26 (not all are visible in the figure), adjusting output, adjusting the cost of goods sold. (Adjustment amounts can also be negative if the actual cost is less than the planned cost).

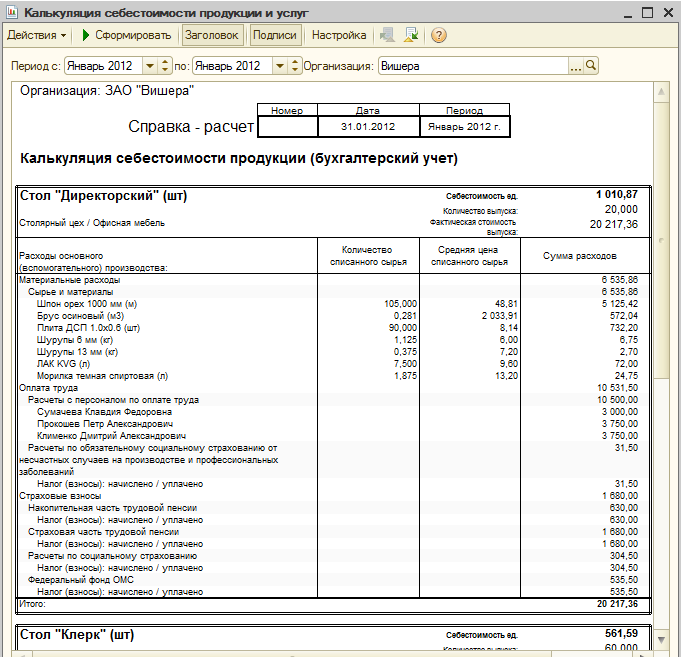

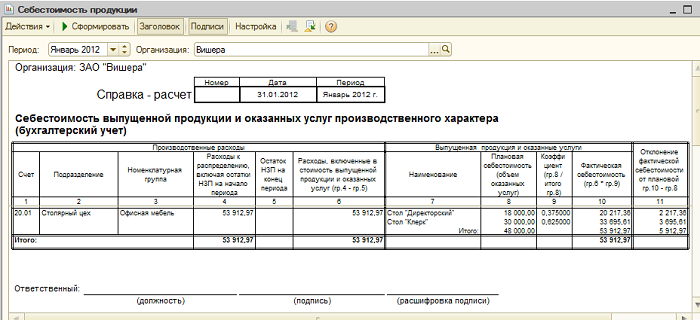

After closing cost accounts, you can generate references-calculations (available from the "Closing of the month" processing or through menu: "Reports - Help-calculations»).

Help-calculation "Calculation":

Help-calculation "Cost of products":

Unfinished production

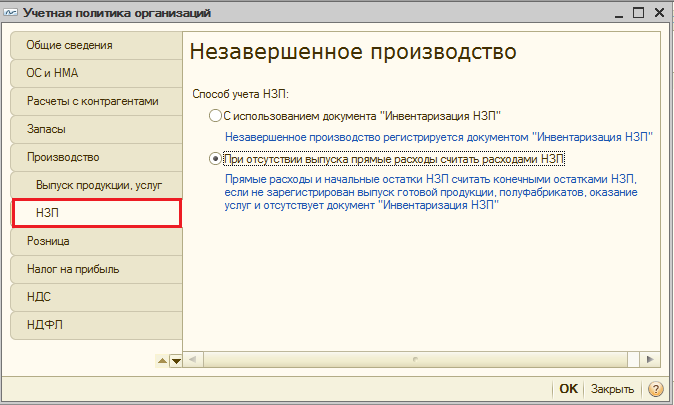

If during the period there were expenses for production, but there was no output (semi-finished products, production services), or it was incomplete, then account 20 is not closed, the cost of work in progress (WIP) remains on it and goes to the next month. Accounting for work in progress can be configured in the form of the organization's accounting policy, on the "WIP" tab. By default, the method “If there is no output, consider direct costs as WIP costs” is usually set:

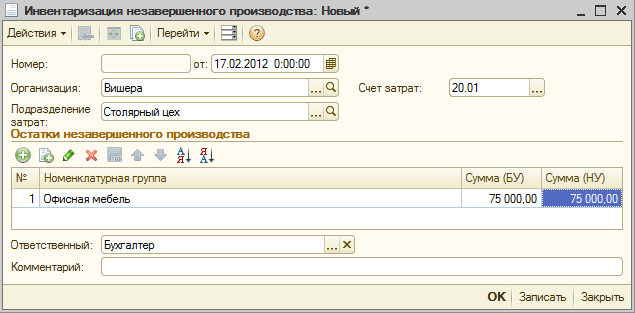

If, in the accounting policy, the WIP accounting method “Using the WIP Inventory document” is selected, then if there is work in progress, it will be necessary to enter the WIP Inventory document before closing the month. Here, the amounts of work in progress for each item group are manually indicated.

02.09.2012

Production costs

Accounting for production costs in the program "1C: Accounting 8" is carried out in the context of product groups (types of activity). Previously, they must be entered in the reference book "Nomenclature groups" ( menu: "Enterprise - Goods (materials, products, services)").

Example:

Direct production costs are accounted for on accounts 20 "Main production" and 23 "Auxiliary production". This includes everything that can be attributed to specific types of manufactured products (semi-finished products, production services): raw materials written off for production, depreciation of capital equipment, wages and taxes from the payroll of production workers, as well as some services.

Ready solutions (ready to install and do not require additional configuration)

During the month, direct costs are reflected in the program with the help of such documents as “Request-invoice”, “Receipt of goods and services” (tab “Services”), “Expense report” (tab “Other”), “Payroll”, as well as regulatory operations "Depreciation and depreciation of fixed assets", "Calculation of taxes (contributions) from payroll" and some others. You should pay attention to the correct indication of the item group both in the documents and in the ways of reflecting depreciation costs and reflecting wages in accounting.

Examples of direct production costs

The document "Requirement-invoice" (menu or tab "Production") reflects the write-off of materials to production. The cost account and analytics are listed on the Cost Account tab. When posting the document, the posting Dt 20.01 Kt 10 will be generated, with the corresponding analytics of account 20 (subdivision, item group, cost item).

The method of reflecting depreciation expenses (menu or tab "OS" or "Intangible assets"). If you choose this method when accepting a fixed asset for accounting (acceptance for accounting of intangible assets, putting work clothes into operation), then depreciation for this asset (depreciation of intangible assets, repayment of the cost of work clothes) will be charged to the specified account and cost analytics. In this case, the posting Dt 20.01 Kt 02.01 will be generated.

Method of reflecting salary in accounting (menu or tab "Salary"). If you specify this method in the accrual, then the employee's salary and payroll taxes will be charged to the corresponding account and cost analytics. In this case, when calculating the salary, the posting Dt 20.01 Kt 70 will be generated.

At the end of the month, direct costs collected on accounts 20 and 23 are distributed between manufactured products and work in progress by item groups (types of activity). Distribution occurs with the help of regular month-end closing operations.

In addition, there are general production and general business expenses, which are accounted for, respectively, on accounts 25 and 26.

General production expenses during the month are charged to account 25. To reflect them, the same documents can be used as for reflecting direct costs. At the end of the month, the costs collected on account 25 are distributed to account 20 by item groups (types of activity), within a specific unit, in accordance with the distribution base, using routine operations.

General business expenses during the month are charged to account 26. To reflect them, the same documents can be used as for reflecting direct costs. At the end of the month, the write-off of expenses collected on account 26 can occur in two ways. They can be distributed to account 20 by item groups (types of activity) of the entire enterprise, in accordance with the selected distribution base. Or, if the "direct costing" method is used, general business expenses are written off directly to account 90.08 "Administrative expenses" in proportion to the sales proceeds.

Cost accounting is set up in the form of the organization's accounting policy (menu or tab "Enterprise").

On the “Production” tab, methods for distributing general and general production costs are indicated using the “Set distribution methods ...” button. In the form that opens, you need to indicate the distribution base for each account, which can be the volume of output, the planned cost of production, wages, material costs, revenue, direct costs, and individual items of direct costs. If necessary, you can detail the methods of distribution by departments and cost items.

Here you can also configure the use of the direct costing method and the distribution of production costs for services.

On the “Product output” tab, a method for accounting for the output of finished products (semi-finished products, production services) is selected - with or without the use of account 40. Here it is also necessary to specify the definition of the sequence of redistribution for closing accounts, which is important in multi-refining production. Selecting automatic detection is recommended. If the output is accounted for at the planned cost using account 40, then automatic calculation of the sequence of redistribution is not possible. In this case, you need to select the manual method, and then manually set the order of departments for closing accounts (by clicking the button).

Automatic determination of the sequence of redistributions is set:

Manual determination of the sequence of redistributions is set, the order of divisions is established:

Release and sale of finished products

The output of products (semi-finished products, production services for sob. subdivisions) is reflected in the program by the document “Report of production for a shift” (menu or tab “Production”). Released products are accounted for at the planned cost, the document generates posting Dt 43 Kt 20 (or, if the use of account 40 is specified, posting Dt 43 Kt 40). You must correctly specify the item group for the released products.

The document "Report of production for the shift" and the result of its implementation (account 40 is not used):

For the correct calculation of the cost in the program, it is necessary to observe the principle of matching income and expenses in the context of product groups (types of activity). That is, if there are costs for an item group, they must correspond to the output and income for this item group.

The sale of finished products is reflected in the document “Sales of goods and services”, while generating a revenue entry: Dt 62 Kt 90.01, and a posting to write off the cost of goods sold: Dt 90.02 Kt 43. Analytics of accounts 90.01 and 90.02 - nomenclature groups (types of activity).

The result of the document for the sale of products:

Closing the period and calculating the actual cost

Closing of cost accounts and calculation of the actual cost of manufactured products (semi-finished products) is carried out at the end of the month by routine operations. Preliminary, routine operations must be performed to accrue depreciation of fixed assets and intangible assets, pay off the cost of workwear, write off deferred expenses, calculate salaries and payroll taxes.

You can use the routine processing "Closing the month" ( menu: "Operations"). In this case, the program itself will “determine” which scheduled operations are necessary and will carry them out in the correct sequence. Execution occurs on the button "Perform closing of the month".

When carrying out the routine operation “Closing accounts 20, 23, 25, 26”, several stages are performed: distribution of indirect costs (according to the established “Distribution Methods”), calculation of direct costs for each product and for each division, cost adjustment.

Let us give an example of the operation “Closing accounts 20, 23, 25, 26” (the organization uses the “direct costing” method). There are postings for closing account 26 (not all are visible in the figure), adjusting output, adjusting the cost of goods sold. (Adjustment amounts can also be negative if the actual cost is less than the planned cost).

After closing cost accounts, you can generate references-calculations (available from the "Closing of the month" processing or through menu: "Reports - Help-calculations»).

Help-calculation "Calculation":

Help-calculation "Cost of products":

Unfinished production

If during the period there were expenses for production, but there was no output (semi-finished products, production services), or it was incomplete, then account 20 is not closed, the cost of work in progress (WIP) remains on it and goes to the next month. Accounting for work in progress can be configured in the form of the organization's accounting policy, on the "WIP" tab. By default, the method “If there is no output, consider direct costs as WIP costs” is usually set:

If, in the accounting policy, the WIP accounting method “Using the WIP Inventory document” is selected, then if there is work in progress, it will be necessary to enter the WIP Inventory document before closing the month. Here, the amounts of work in progress for each item group are manually indicated:

The latest releases of edition 4.5 of the 1C: Accounting program have significantly expanded the possibilities for automating various areas of accounting. The section "Release of finished products" did not remain without attention. In the proposed article, the leading consultant of the training center "Master Service Engineering" E.A. Denisova tells how best to take into account finished products in 1C: Accounting.

In the "1C: Accounting" configuration, the method of accounting for finished products is set by a periodic constant in the "Operations" menu, which is called "Method of accounting for finished products and semi-finished products". By default, the value "At actual cost" is set, since it is this accounting method that complies with the norm of paragraph 5 of PBU 5/01 "Accounting for inventories", approved by order of the Ministry of Finance of Russia dated 09.06.2001 No. 44n. Another value ("By planned cost") is left as a reserve for cases if the configuration will be used to restore accounting for 2001, when PBU 5/01 has not yet come into effect. In our article, we will consider how the method of accounting "at actual cost" is implemented in practice.

Before starting work with the program, it is necessary to fill in the reference book "Types of products, works, services", defining for each element of the reference book the "Type of nomenclature" (for finished products - this is "Product", respectively). An example of directory organization is shown in fig. 1.

The elements of this directory are objects of analytical accounting on account 20 (subconto 1). During the month, production costs are collected on the debit of account 20 for each type of product and for cost items. In order for production costs to be attributed to the cost of a certain type of finished product, in all directories and documents where account 20 is used, it is necessary to indicate the type of product in the cost of which these costs should be included. For example, when filling out the "Employees" directory for employees directly involved in the production process, it is necessary to indicate the cost of which product the wages of a particular employee are related to. As can be seen from Fig. 2, Andrei Ivanovich Antonov's salary and tax deductions from his salary will be charged to the cost of paving slabs. The directory "Fixed assets" is filled in the same way. As a result, depreciation is charged to the cost of production, in the production of which this fixed asset participates.

We suggest that you consider the method of accounting for finished products at actual cost using the example of an enterprise that produces several types of products.

Example

LLC "Krona" produces several types of finished products: curbs and paving slabs.

During the month, materials were purchased in the amount of 171,100 rubles. (including VAT 18% - 26,100 rubles). Items released:

- for the production of borders - in the amount of 2,500 rubles;

- for the production of paving slabs - in the amount of 82,500 rubles.

The company used the services of a third-party organization to transport finished products (curbs) from the workshop to the warehouse - 1,770 rubles. (including VAT 18% - 270 rubles). Within a month, the finished products were shipped to the buyer:

- sidewalk curb - 100 pcs. 150 rub. = 15,000 rubles. (without VAT)

- paving slabs "Hexagon" - 500 pcs. 130 rub. = 76,700 rubles. (without VAT)

- paving slabs "Herringbone" - 100 pcs. 400 rubles each = 40,000 rubles. (without VAT).

Let's consider successively the stages of the production cycle:

- Issue of materials to production.

- Third-party company services.

- Output.

- Sales of finished products.

- Closing of the month.

1. Issue of materials to production.

The release of materials into production is carried out by the document "Movement of materials". In the document, the type of transfer "Transfer to production", the account for allocating costs 20 and the type of item to which the materials are transferred are selected. Below are the postings that are generated during the document (in our case, the release of materials for the production of paving slabs):

Debit 20 "Main production" Credit 10.1 "Raw materials" - 30,000 rubles. - transferred to production (paving slabs) material - Expanded clay 300 m3 for 100 rubles. Debit 20 "Main production" Credit 10.1 "Raw materials" - 45,000 rubles. - transferred to production (paving slabs) material - Dye 300 kg at 150 rubles. Debit 20 "Main production" Credit 10.1 "Raw materials" - 7,500 rubles. - transferred to production (paving slabs) material - sand 150 m3 for 50 rubles.

2. Third Party Services.

The company used the services of a third-party organization to transport finished products (curbs) from the workshop to the warehouse - 1770 rubles. (including VAT 18% - 270 rubles). These services were included in the cost of curbs. In the "Third Party Services" document, account 20 is selected as the offsetting account, and the border is selected as subconto 1. As a result of posting the document, postings will be generated:

Debit 20 Credit 60/76 - 1,500 rubles. - services for the transportation of finished products Debit 19 Credit 60/76 - 270 rubles. - accepted for VAT offset.

3. Product release.

In a month, finished products were produced:

- sidewalk curb - 100 pcs. 120 rub. = 12,000 rubles.

- paving slabs "Hexagon" - 500 pcs. for 105 rubles. = 52,500 rubles.

- paving slabs "Herringbone" - 100 pcs. for 390 rubles. = 39,000 rubles.

The release of products is carried out in the program by the document "Transfer of finished products to the warehouse" (Fig. 3)

Arriving at the warehouse of finished products within a month, we do not always know its actual cost (for example, wages and depreciation will be charged to costs only at the end of the month), so finished products are brought to the warehouse at the planned cost ("Cost" column of the document). To automatically enter the planned cost into the document in the "Nomenclature" reference book, the released products must have the "Planned cost price" attribute filled in, that is, the approximate amount of costs for the production of one unit of this product.

When calculating the cost of production, the postings will be generated based on the planned cost specified in the document, in our example, the documents "Transfer of finished products to the warehouse" will form the postings:

Debit 43 "Finished products" Credit 40 "Product release" 12,000 rubles. - Border 100x30x70 (100 pieces for 120 rubles); Debit 43 "Finished products" Credit 40 "Product output" 52,500 rubles. - Paving slabs "Hexagon" (500 pieces for 105 rubles); Debit 43 "Finished products" Credit 40 "Product release" 39,000 rubles. - Paving slabs "Herringbone" (100 pieces for 390 rubles).

4. Sales of finished products.

Within a month, the finished product was shipped to the buyer:

- sidewalk curb - 100 pcs. 150 rub. = 15,000 rubles. (without VAT)

- paving slabs "Hexagon" - 500 pcs. 130 rub. = 76,700 rubles. (without VAT)

- paving slabs "Herringbone" - 100 pcs. 400 rubles each = 40,000 rubles. (without VAT).

To do this, a document "Shipment of goods, products" is created. In the document, in the "Price" column, the selling price is indicated, while postings are generated:

Debit 90.2.1 "Cost of sales not subject to UTII" Credit 43 "Finished products" - 12,000 rubles. - shipped from the warehouse finished products at a cost of 100 pcs. 120 rubles each Debit 62.1 "Settlements with buyers and customers (in rubles)" Credit 90.1.1 "Revenue from sales not subject to UTII" - 17,700 rubles. - reflected the proceeds from the sale

5. Closing of the month.

The closing of the month is the final stage of the production cycle, the document that closes accounts 20 and 40, which, in the absence of work in progress, should not have balances at the end of the month. It would not be superfluous to recall that before the formation of the "Closing of the month" document, it is necessary to post all the documents that form postings to the debit of account 20, including payroll and depreciation. On fig. 4 shows the document "Closing the month", which should be carried out when writing off finished products at actual cost.

When performing the action "Calculation and adjustment of the cost of GP and PF" (which is performed when posting a document at the end of the month):

- Account 20 is closed in the debit of account 40 in terms of expenses attributable to the cost of products released in the current month;

- Direct costs are allocated to the cost of manufactured products (write-off from account 40);

- Adjustment of write-offs of products to their actual cost.

In our example, the document "Closing the month" will generate postings:

Debit 40 Credit 20 - 888.89 - closing account 20 (Border, Depreciation) Debit 40 Credit 20 - 1,080.00 - closing account 20 (Border, UST) Debit 40 Credit 20 - 5,000.00 - closing account 20 (Border , Salary) Debit 40 Credit 20 - 2,500.00 - account closing 20 (Border, Material costs) Debit 40 Credit 20 - 1,500.00 - account closing 20 (Border, Third Party Services) Debit 40 Credit 20 - 700, 00 - closing account 20 (Border, FSS from NS and PZ) Debit 40 Credit 20 - 1,512.00 - closing account 20 (Paving slabs, UST) Debit 40 Credit 20 - 7,000.00 - closing account 20 (Paving slabs, Salary) Debit 40 Credit 20 - 82,500.00 - closing account 20 (Paving slabs, Material costs) Debit 40 Credit 20 - 980.00 - closing account 20 (Paving slabs, FSS from the National Assembly and PZ) Debit 43 Credit 40 ( reversal) - 331.11 - Adjustment of output (Border 100x30x70) Debit 90.2.1 Credit 43 (reversal) - 331.11 - adjustment of the cost of production (Border 100x30x70) Debit 43 Credit 40 - 209.70 - adjustment of output (Paving slabs "Herringbone") Debit 90.2. Credit 43 - 209.70 - adjustment of the cost of production (paving slab "Herringbone") Debit 43 Credit 40 - 282, 30 - adjustment of output (paving slab "Hexagon") Debit 90.2.1 Credit 43 - 282.30 - adjustment of the cost of production (Slabs paving "Hexagon")

When posting the document "Closing the month" with the checkbox "Generate a report when posting the document" checked, you can generate a report that will allow us to consider in detail how the cost of finished products was calculated and adjusted. In the month-end report, the rows that are highlighted in darker color and underlined are the so-called "links" that can be opened with a mouse click (Fig. 5).

In our example, the lines "Calculation of the cost of manufactured products and semi-finished products" and "Adjustment of the cost of products and semi-finished products" will be underlined. Thus, you can see how the program calculated the cost of production (Fig. 6).

The data of this report is the same as the analysis of account 20 by subconto, but presented in a more visual form. In addition, the amount of direct costs that "fell" on the cost of each type of product by cost items can be deciphered by double-clicking in column 4 of the corresponding line of the table (Fig. 7).

The report in Figure 7 shows the reflection of direct costs in the context of cost items (turnovers D40-K20 by type of product).

Column 7 can also be deciphered by double-clicking a mouse, and a report is obtained by type of product, where its planned and actual cost is compared.

The report on the adjustment of write-off operations is presented in fig. 8.

A negative adjustment is obtained if the planned cost of output (which we indicated in the "Product output" document) exceeds the actual amount of costs for the release of this product, a positive one - if the amount of costs for output exceeds the planned cost of output.

Sales of products- one of the main business operations of a manufacturing enterprise.

The correct reflection of this operation is of great importance for the formation of the cost of production, and therefore it is important to follow the basic principles.

First, the program must follow the correct chronological sequence of entering documents - i.e. the receipt of products at the warehouse must be done earlier than its sale.

Secondly, the write-off of products should occur from the warehouse to which they were credited (or moved).

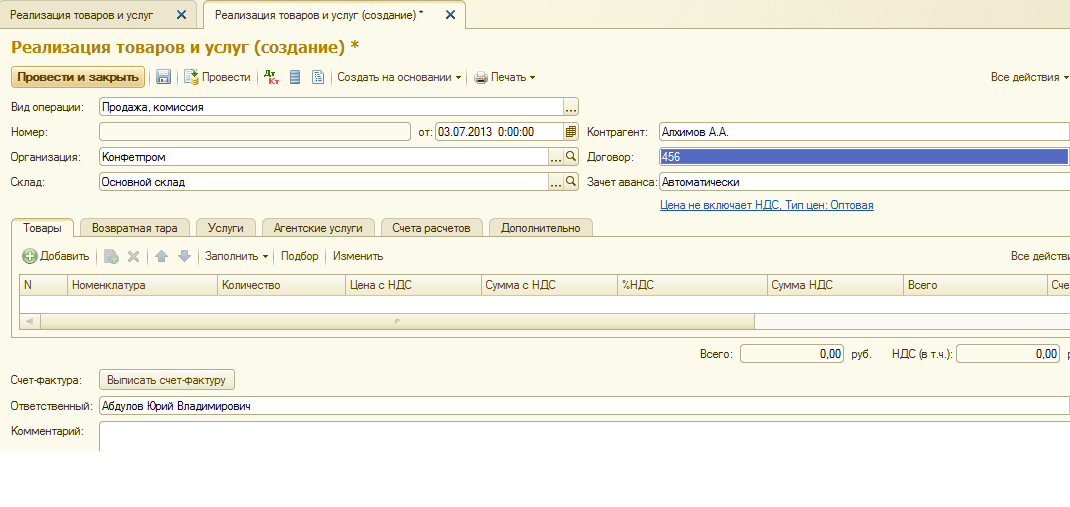

To reflect the sale of products in the program 1C Accounting 8 the document "Sales of goods and services" is used.

You can find the list of documents “Sales of goods and services” in the section “Purchases and sales”, subsection “Sales”, link “Sales of goods and services”.

A new document form will open.

The type of operation is indicated "Purchase, commission".

The "Organization" attribute will be filled in automatically if the main organization is specified in the user's settings or the system records only one organization.

In the "Warehouse" attribute, select the warehouse from which we sell the products.

We select a counterparty-buyer, or enter it in the "Counterparties" directory if we sell products to this buyer for the first time.

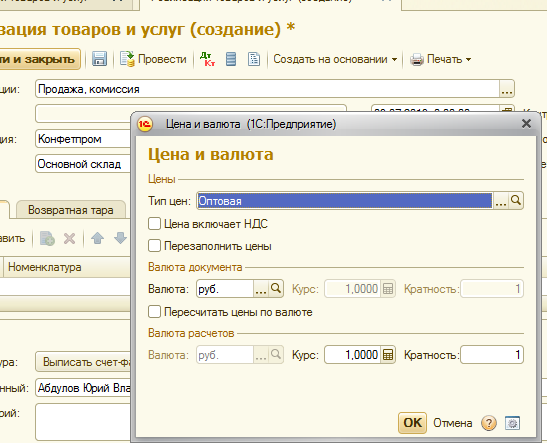

We enter an agreement with a counterparty. It is important to correctly indicate the type of contract - "with the buyer". If we want the same price type to be always indicated in the sales documents for this buyer, we select this price type in the contract (for this, the required price type must be entered in the "Nomenclature price types" reference book).

The “Advance payment offset” attribute can be set to “do not read out” (i.e. advance payment entries are not generated even if there is a buyer’s prepayment), “automatically” (i.e. the program analyzes the presence of an advance payment for this buyer and the contract) and “according to the document” (in this case, you must specify the advance payment document). The default value is "automatic", I recommend leaving it in this position.

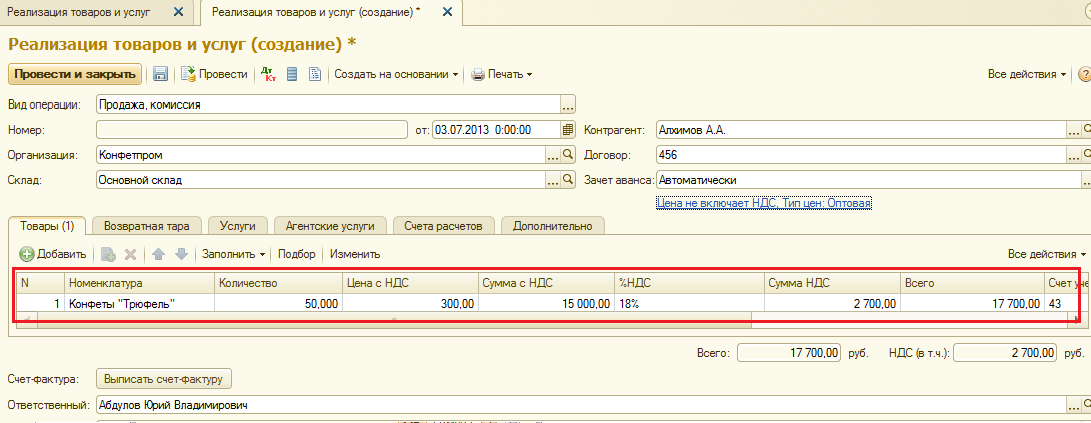

We fill in the tabular part of the document from the reference book "Nomenclature" using the button ". Specify the number of products.

If pre-filled, then when you select an item in the line, the accounting account, VAT account, income and expense accounts for the sale of this product will be automatically filled in.

If the prices for products are not filled in for the previously specified price type, then you will have to enter the sales price of products manually.

Depending on the settings made earlier, the VAT amount will be automatically calculated.

Using the button "Issue an invoice", you can generate the document "Issued invoice" on the basis of this document.

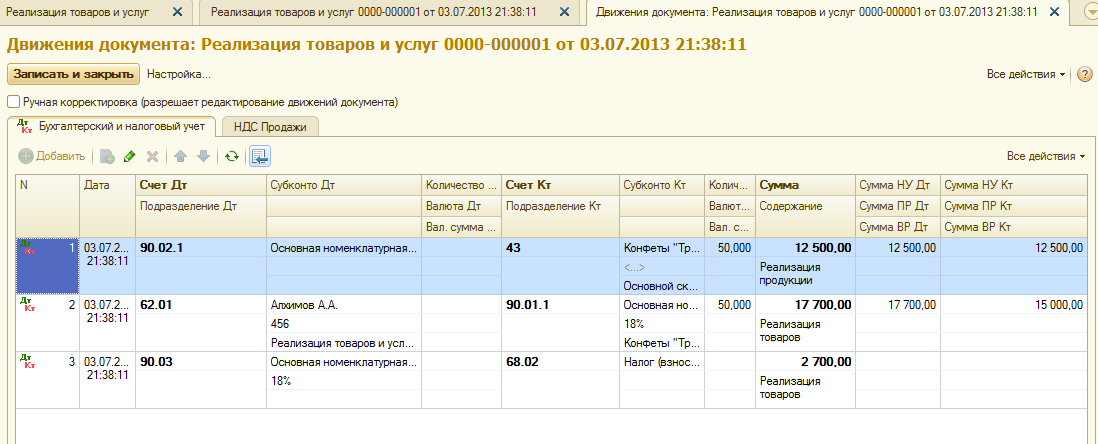

After entering all the details, we conduct the document. We look at the postings generated by the document:

Posting debit 90.02, credit 43 reflects the write-off of products at the planned cost.

The second entry reflects the sale of products at the selling price, including VAT.

The third entry is the VAT amount.

The "Print" button opens a list of printable forms that can be generated from this document.

For this operation, the forms “Invoice”, “Invoice”, “Consignment note (TORG-12)”, “Consignment note 1-T” and “Consignment note” are suitable for us.

To learn how to properly set up the signatures of responsible persons so that they are displayed automatically in printed forms of a document, read